In our last blog post we learned that one of the primary culprits behind a prohibited transaction with your self-directed IRA is the involvement of a Disqualified Person. Expanding on prior content we took a deeper dive to provide you with the following information.

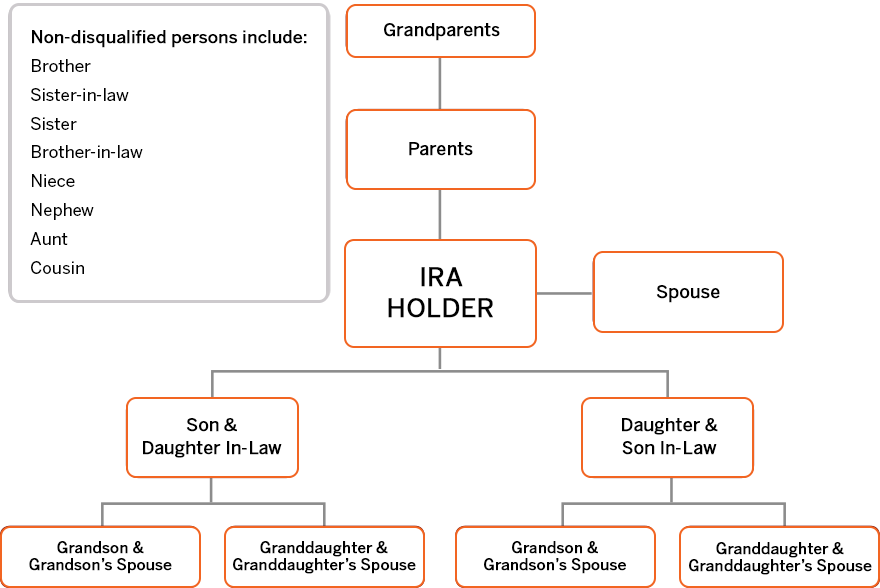

First, let’s begin with the primary reference source, the Internal Revenue Service. IRS Publication 560 outlines in detail who/what constitutes a Disqualified Person. That being said, much of what we find in IRS Publications can be difficult to understand, but we found this graphic from our friends at New Direction and found it super helpful to provide guidance:

Basically, anyone in relation or in close touch with the IRA account holder may not qualify to access the funds in the account. Here is the list of disqualified people:

- You, the account owner

- A beneficiary of the IRA

- Your spouse

- Your lineal ascendants/descendants and their spouses

- Plan service providers and fiduciaries (including advisors, custodians, and administrators)

- An entity (corporation, estate, partnership, etc.) in which you own at least 50% of the voting stock, directly or indirectly.

- An officer, director or a 10% or more share holder or partner.

You may be wondering what exceptions may exist from this list. Here are some that we found:

- Brother or sister of the IRA account owner

- Cousin of the IRA account owner

- Spouse’s parents (in-laws)

- Step-parents or step-grandparents

- Aunt or Uncle of the IRA account owner

- Niece or Nephew of the IRA account owner

- Friends of the IRA account owner

As with Prohibited Transactions, we would always recommend that you seek professional guidance prior to initiating an investment with your self-directed IRA. This ensures the integrity of your IRA investments.

Recent Comments