The world of Self-Directed IRAs (SDIRAs) offers a wide variety of investment options, including real estate. However, the Account Holder, Custodian, and Non-Recourse Lender must work as a team to avoid prohibited transactions. One of the most commonly observed culprits of a prohibited transaction comes through the involvement of a “Disqualified Person.”

Understanding who qualifies as a Disqualified Person and how this classification affects your investment decisions is essential for maintaining IRS compliance and avoiding prohibited transactions.

But first, we need to answer the basics.

So Who Is A Disqualified Person, Anyway?

A Disqualified Person is an individual or entity that is restricted by IRS rules from engaging in certain transactions with your Self-Directed IRA. These restrictions are put in place to prevent any conflicts of interest and to ensure that the IRA is used primarily for retirement savings – not for personal benefit.

Key Categories of Disqualified Persons:

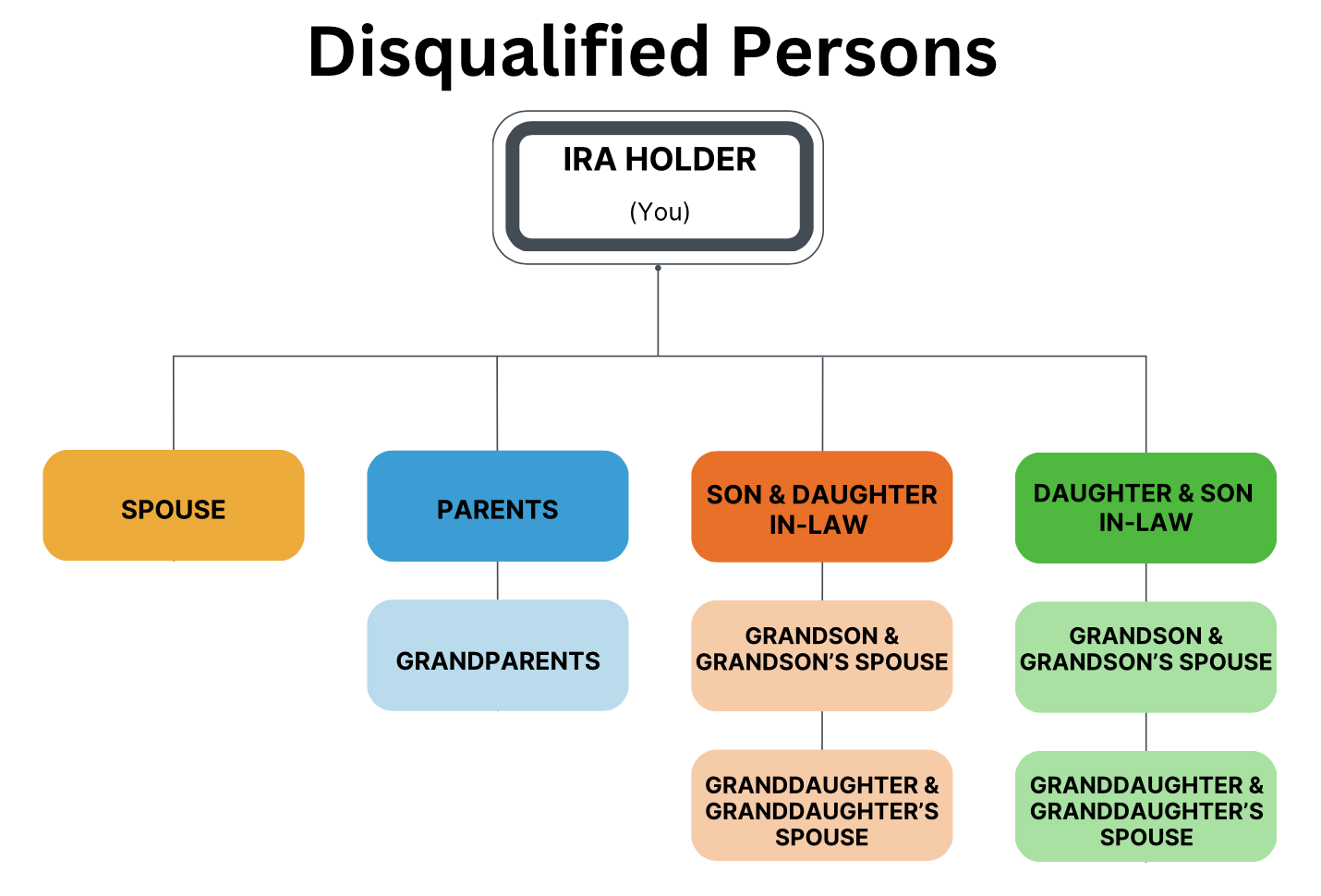

The IRA Owner: You, the account holder, are considered a Disqualified Person with respect to your own IRA. This means you cannot directly benefit from or engage in transactions that provide you with immediate gains.

Certain Family Members: Immediate family members, including your spouse, children, parents, and any of their spouses, are also considered Disqualified Persons. This rule also extends to lineal descendants and their spouses, so keep that in mind.

Entities: Any business or entity in which you (the IRA owner) have a significant ownership interest is classified as a Disqualified Person. This includes companies you control or have a stake in, as well as businesses where your family members hold key positions such as Financial Officer.

Certain Service Providers: Certain professionals and advisors who provide services to your IRA, such as attorneys, accountants, or brokers, can also be considered Disqualified Persons, especially if they are involved in transactions related to the IRA.

Why Does the Concept of A Disqualified Person Matter?

Understanding who qualifies as a Disqualified Person is crucial because engaging in transactions with these individuals or entities can lead to what the IRS defines as a Prohibited Transaction. A Prohibited Transaction can result in substantial tax consequences, including the potential disqualification of your IRA and significant penalties.

In the realm of Self-Directed IRAs, the concept of a Disqualified Person is essential for maintaining compliance and ensuring your retirement investments are properly managed. By adhering to these regulations and avoiding prohibited transactions, you can protect your IRA and optimize your investment strategies.

For more detailed guidance, you should always consider consulting with your chosen IRA Custodian who is experienced in SDIRA management as well as reading up on the latest IRS rules to educate yourself.

Explore Your Options with Peak

If you’re interested in exploring non-recourse loan options for your Self-Directed IRA, Peak Asset Lending specializes in providing these unique financial solutions.

Contact Our Team to learn how we can assist you in maximizing your investment potential while ensuring compliance with every regulation.

Recent Comments